Extraordinary Fundamentals, Narratives Not So Much

- Feb 12

- 6 min read

Financial markets are rarely neutral observers of reality. They interpret, exaggerate, simplify, and often distort. Prices are shaped less by what companies earn today and more by what investors collectively believe about tomorrow. This dynamic creates a recurring phenomenon: companies with strong fundamentals trading at discounted valuations because the prevailing narrative has turned against them.

This article explores that disconnect. It examines how market narratives can overpower financial performance, why this happens repeatedly, and how it creates opportunities for long-term investors. To illustrate this dynamic, we focus on three companies that, despite extraordinary fundamentals, have suffered from uninspiring or outright negative narratives: PayPal, Adobe, and Salesforce.

These are not turnaround stories. They are cases where the business continues to perform, but the market’s attention has moved elsewhere.

The Gap Between Fundamentals and Narrative

Markets thrive on stories. Stories are easier to understand than balance sheets, more emotionally compelling than cash flow statements, and more shareable than operating margins. When a story resonates, capital flows. When it doesn’t, even excellent companies can be left behind.

Narratives often emerge from real concerns, but they tend to extrapolate those concerns indefinitely. A growth slowdown becomes a “broken business.” Increased competition becomes “structural decline.” Strategic reinvestment becomes “margin pressure.” Over time, repetition turns interpretation into perceived fact.

This gap between fundamentals and narrative is not a flaw of markets. It is a feature. And it is precisely where disciplined investors can find opportunity.

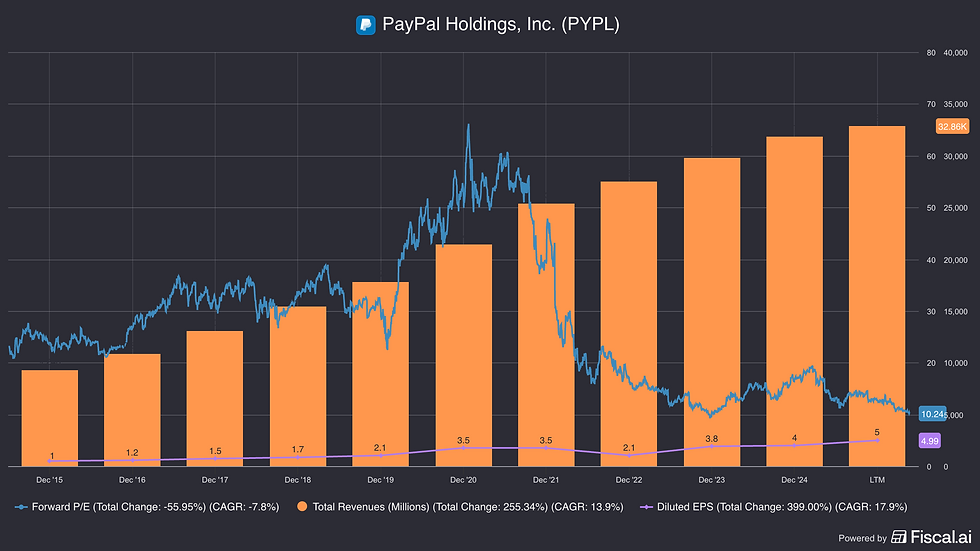

PayPal: A Profitable Platform Trapped in a Growth Narrative

PayPal’s narrative problem began when growth slowed. For years, the company was treated as a high-growth fintech disruptor, priced accordingly and compared to early-stage innovators. When transaction growth decelerated and competition intensified, the market rapidly rewrote the story.

Suddenly, PayPal was no longer a growth platform but a “legacy payments company.” The narrative shifted toward fears of commoditization, pressure from Apple Pay and other digital wallets, and the assumption that PayPal’s relevance was fading.

Yet the fundamentals told a very different story.

PayPal remains one of the largest digital payments platforms globally, with hundreds of millions of active users and enormous transaction volume. The company generates substantial free cash flow, maintains healthy operating margins, and has a deeply embedded position in global e-commerce. Slower growth did not mean declining economics. It meant maturation.

What the market struggled to accept was that PayPal had transitioned from a story stock to a cash-flow business. Investors anchored to the old narrative of hypergrowth failed to reframe the company as a durable payments infrastructure provider. As a result, valuation multiples compressed dramatically, even as profitability and cash generation remained strong.

PayPal’s case highlights a common market mistake: confusing slower growth with deteriorating quality. In reality, many of the world’s best businesses eventually trade growth for durability. The market often penalizes that transition before recognizing its long-term value.

Adobe: From Subscription Success to AI Anxiety

Adobe presents a different but equally instructive example. The company executed one of the most successful business model transitions in software history, moving from perpetual licenses to a subscription model that dramatically increased recurring revenue, visibility, and margins.

For years, this transformation was celebrated. Adobe became synonymous with pricing power, high margins, and sticky enterprise customers. Its fundamentals remained exceptional, with strong revenue growth, operating leverage, and free cash flow generation.

Then the narrative shifted.

The emergence of generative AI tools sparked concern that Adobe’s creative software moat could be eroded by cheaper, AI-native alternatives. Investors began to question whether Photoshop, Illustrator, and Premiere would remain indispensable in a world where content creation could be automated or simplified. Once again, the narrative ran ahead of the numbers.

Adobe did not stand still. It integrated AI directly into its ecosystem, embedding generative tools in ways that enhanced productivity rather than replacing professionals. Its customer base continued to grow, pricing power remained intact, and margins stayed robust. Yet the stock experienced periods of underperformance as fear dominated interpretation.

This disconnect reveals another psychological trap: assuming disruption automatically destroys incumbents. History suggests the opposite is often true. Incumbents with distribution, brand trust, and enterprise relationships are frequently best positioned to monetize new technologies.

Adobe’s fundamentals never stopped being extraordinary. What changed was the story investors told themselves about the future of creativity.

Salesforce: When Size Becomes a Narrative Liability

Salesforce’s challenge is not relevance, but scale. As the dominant player in customer relationship management software, Salesforce has become a victim of its own success. Growth inevitably slowed as the business matured, and investors began to question whether innovation and expansion could continue at the pace expected of a premium-valued tech company.

The narrative evolved from admiration to skepticism. Salesforce was no longer seen as a growth engine but as a bloated software conglomerate struggling to integrate acquisitions and defend margins. Headlines focused on cost structure, activist pressure, and internal restructuring rather than customer retention or recurring revenue.

Yet beneath the narrative, Salesforce continued to demonstrate extraordinary fundamentals. Recurring subscription revenue remained strong. Customer lock-in was deep. Switching costs were high. Free cash flow improved as management responded to shareholder concerns with greater cost discipline.

What the market overlooked was that Salesforce was transitioning into a different phase of its lifecycle. Like PayPal, it was moving from expansion to optimization. Like Adobe, it was integrating new technologies into an established platform rather than being displaced by them.

Salesforce illustrates how size itself can become a narrative headwind, even when it brings stability, pricing power, and scale advantages. Markets often romanticize disruption but undervalue consolidation.

Why Narratives Drift Away from Fundamentals

The cases of PayPal, Adobe, and Salesforce share a common psychological pattern. Each company experienced a shift in narrative that was disproportionate to changes in economic reality. This happens for several reasons.

Markets anchor to past growth rates and struggle to recalibrate expectations. When reality fails to match previous trajectories, disappointment sets in even if performance remains strong.

Investors also prefer simple stories. “Growth is slowing” is easier to process than “growth is normalizing while margins and cash flow improve.” Simplicity wins attention, even when it loses accuracy.

Finally, capital rotates. When new themes emerge, such as artificial intelligence or emerging technologies, attention and capital migrate. Companies outside the dominant narrative are not necessarily flawed. They are simply unfashionable.

The Cost of Ignoring Fundamentals

Ignoring fundamentals has consequences. Over time, valuation gaps tend to close. Either fundamentals deteriorate to justify pessimism, or prices recover to reflect economic strength. In the cases discussed here, deterioration has not materialized.

PayPal continues to generate cash at scale. Adobe remains deeply embedded in creative and enterprise workflows. Salesforce maintains a dominant position in CRM with expanding profitability.

When narrative pessimism becomes embedded in pricing, the risk profile changes. Downside becomes limited by cash flow and balance sheet strength, while upside emerges from even modest narrative improvement. The market does not require perfection. It only requires reality to be slightly better than feared.

Why These Situations Matter for Long-Term Investors

For long-term investors, opportunities rarely arise when narratives are positive and confidence is high. They emerge when expectations are compressed and stories are stale.

The challenge is psychological rather than analytical. Buying companies with extraordinary fundamentals but uninspiring narratives requires patience and conviction. It requires accepting that price may not move immediately, and that headlines may remain negative longer than expected.

Yet history consistently shows that cash-generating businesses with durable advantages eventually reassert themselves. The timing is uncertain, but the direction is often clear.

Reframing the Question

The key investment question is not whether PayPal, Adobe, or Salesforce will return to peak valuation multiples. It is whether their current valuations accurately reflect their long-term earning power.

If the answer is no, then the narrative has created opportunity rather than risk.

Markets will always chase the next story. They will always overreact to change and underreact to durability. Understanding this dynamic is one of the most valuable skills an investor can develop.

When Stories Fade and Numbers Remain

Extraordinary fundamentals do not guarantee immediate returns. But they do anchor long-term value. PayPal, Adobe, and Salesforce demonstrate how easily markets can lose sight of economic reality when narratives shift. None of these companies lost relevance. None experienced structural collapse. What they lost, temporarily, was investor imagination.

In time, imagination returns to where cash flows persist.

For investors willing to look beyond fashionable themes and temporary sentiment, these situations offer a powerful reminder: stories move prices in the short term, but fundamentals determine outcomes in the long term. When narratives disappoint but fundamentals endure, patience is not just a virtue. It is a strategy.

Comments