PAYPAL (PYPL)

PayPal Holdings, Inc. operates a technology platform that enables digital payments for merchants and consumers worldwide. It operates a two-sided network at scale that connects merchants and consumers that enables its customers to connect, transact, and send and receive payments through online and in person, as well as transfer and withdraw funds using various funding sources, such as bank accounts, PayPal or Venmo account balance, consumer credit products, credit and debit cards, and cryptocurrencies, as well as other stored value products, including gift cards and eligible rewards.

This investment thesis does not constitute a buy or sell recommendation. Each investor should conduct their own research and be responsible for their actions. This document clearly and objectively summarizes a specific viewpoint.

We are not liable for any negligence. This investment thesis was created by ZIIX Growth™ and is therefore protected by copyright. Its use, distribution, and commercialization are reserved for the company; the document may not be modified.

INTRODUCTION

PayPal remains one of the most influential and misunderstood players in the global digital payments ecosystem. Despite its established brand, robust cash generation, and vast transaction network, market sentiment has turned cautious over the last two years, largely driven by fears of slowing growth, competitive pressures from newer fintechs, and execution uncertainty.

The core of the investment case centers on a company transitioning from pure transaction volume expansion toward profitable, disciplined growth, under the leadership of CEO Alex Chriss, who has reshaped the executive team and refocused the business on operational efficiency, capital returns, and reaccelerating growth across key platforms such as Braintree, Venmo, and branded checkout. The near-term catalysts lie in potential guidance upgrades, margin expansion, and accelerated share repurchases, while the long-term story rests on PayPal's ability to remain a central node in the global payments infrastructure, particularly in e-commerce and peer-to-peer digital transfers.

COMPETITORS IN THE PAYMENT SECTOR

-

Stripe: A fast-growing fintech company focused on online payment processing for businesses of all sizes, known for its developer-friendly platform and global reach.

-

Square (Block, Inc.): Provides point-of-sale solutions, peer-to-peer payments through Cash App, and small business financial services, competing with PayPal in both consumer and merchant segments.

-

Adyen: A European-based payment processor serving global merchants, offering integrated solutions for online, in-store, and mobile payments.

-

Apple Pay / Google Pay: Mobile wallet and digital payment services that allow consumers to make seamless, contactless payments, increasingly adopted by merchants and users, posing a growing threat in digital payments.

BUSINESS MODEL

-

PayPal operates primarily as a digital payments platform, facilitating online money transfers between consumers, merchants, and businesses. Its business model generates revenue mainly through transaction fees, which are charged to merchants and, in some cases, to consumers for certain types of transactions.

-

PayPal earns interest and fees from its credit products, including “PayPal Credit” and “Buy Now, Pay Later” services, as well as from its Venmo peer-to-peer app and merchant services like invoicing and payment processing. The company benefits from network effects: as more users join, merchants are incentivized to accept PayPal, and vice versa.

Its model is highly scalable, with limited incremental costs per additional transaction, but it faces pressure from competition, regulatory scrutiny, and shifts in digital payment preferences. Overall, PayPal’s business model is focused on facilitating seamless, secure digital transactions while diversifying revenue streams beyond pure transaction fees.

PAYPAL'S INCOME STATEMENT

COMPETITIVE ADVANTAGES

-

Brand Recognition and Trust: PayPal is one of the most recognized digital payment brands worldwide. Consumers and merchants alike associate it with secure, reliable transactions, which lowers friction for adoption compared to newer or lesser-known competitors.

-

Network Effects: The platform benefits from a two-sided network: the more consumers use PayPal, the more attractive it becomes for merchants, and vice versa. This creates a reinforcing cycle that makes it harder for new entrants to achieve the same level of reach.

-

Global Reach and Cross-Border Capabilities: Operating in over 200 markets and supports multiple currencies. Its infrastructure enables international transactions more easily than many regional competitors, giving it an edge in cross-border e-commerce.

-

Diverse Product Ecosystem: Beyond basic payments, PayPal offers products like Venmo, Braintree, PayPal Credit, and Buy Now, Pay Later. This diversification allows it to capture different customer segments and reduce dependency on single revenue source.

-

Data and Fraud Management: PayPal has built sophisticated systems for fraud detection, risk assessment and compliance. This protects both consumers and merchants and acts as a barrier for competitors who may struggle to match its scale and data-driven insights.

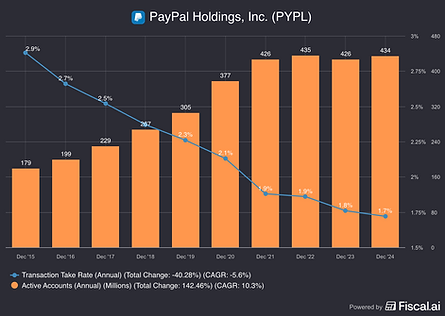

CONSTANT INCOME GROWTH

PayPal has demonstrated relatively consistent revenue growth over the past several years, driven by increasing adoption of digital payments and expanding use of its platform by both consumers and merchants. Growth has been supported by its diversified product suite, including Venmo, merchant services, and credit offerings, which allow it to capture multiple revenue streams.

Even as competition in the fintech space intensifies, PayPal’s established user base, global reach, and scalable infrastructure have contributed to steady income expansion, reflecting the company’s ability to leverage network effects and capitalize on the ongoing shift toward digital transactions.

PAYPAL BUBBLE 2021

PayPal experienced a significant valuation bubble in 2021, driven by the pandemic-era surge in e-commerce and digital payments that created unrealistic expectations about its long-term growth trajectory. At its peak, the company traded at extremely high multiples, reflecting investor optimism that the accelerated digital adoption seen would become permanent. When growth normalized post-pandemic and competitive pressures increased, the stock corrected sharply, wiping out a large portion of those gains.

This dramatic rise and fall has had a lasting psychological impact on many investors. For some, the long decline on the price chart serves as a warning sign, creating a sense of hesitation or distrust even as fundamentals stabilize. The memory of the bubble can make potential investors more cautious, causing them to question whether PayPal can return to sustainable growth or if it remains a “broken growth story.”

PAYPAL PLATFORM

PayPal’s core platform remains the financial engine of the entire company and continues to be its most important source of cash flow. The traditional PayPal checkout experience, where consumers pay merchants using their PayPal account, generates meaningful revenue through transaction fees, currency conversions, and value-added services such as fraud protection and merchant tools. Even as the competitive landscape has pushed the company to lower certain fees and shift toward more unbranded processing, the PayPal-branded checkout still carries significantly higher margins and is the foundation of PayPal’s profitability. This high-quality cash flow is crucial because it provides the financial stability that allows the company to reinvest in new initiatives without jeopardizing its balance sheet.

The cash generated from the PayPal platform funds innovation across the organization, giving the company the ability to experiment with new features, improve infrastructure, and develop additional revenue streams. Whether it’s enhancing security systems, upgrading user experience, or investing in emerging technologies, the platform’s consistent cash generation serves as the backbone of PayPal’s broader strategy. Even though user growth has slowed, the existing base remains highly active and continues to drive strong payment volume, making the PayPal app a reliable and essential operating asset. For the company’s long-term evolution, maintaining a healthy and cash-producing PayPal platform is critical. It finances expansion into new products and allows PayPal to innovate while preserving financial stability.

WHAT'S NEXT FOR PAYPAL?

Looking ahead, PayPal is pursuing multiple initiatives to reignite growth and expand its ecosystem. Venmo remains a central focus, as the company continues to monetize its large, engaged user base through merchant payments, in-app purchases, and its Venmo credit card. The BNPL (Buy Now, Pay Later) segment is also expected to play a growing role, particularly as consumer demand for flexible payment options continues to rise globally.

In addition, PayPal is exploring the potential of cryptocurrencies and stablecoins, aiming to position itself as a bridge between traditional finance and the emerging digital asset economy. This includes enabling crypto transactions and potentially integrating blockchain-based solutions into its payment platform. The partnership with OpenAI could further enhance PayPal’s competitive edge by introducing AI-driven personalization, fraud prevention, and smarter financial tools for both consumers and merchants.

The company is also experimenting with advertising within its ecosystem, allowing merchants to promote products and offers directly to users, which could open a new revenue stream while strengthening engagement on its platforms. Together, these initiatives reflect a multi-pronged strategy to drive growth, diversify revenue, and ensure that PayPal remains a leading innovator in the fast-evolving digital payments landscape.

VENMO, A HIDDEN GEM

Venmo, a subsidiary of PayPal, is often described as a “hidden gem” because of its strong position in the peer-to-peer (P2P) payments space and its potential for future monetization. Originally launched as a mobile app for splitting bills and sending money between friends, Venmo has grown into a widely used platform with millions of active users, particularly among younger demographics. Its social feed and user-friendly interface create a sticky experience that encourages frequent engagement, giving PayPal access to rich behavioral data and a highly engaged user base.

Beyond P2P transfers, Venmo has expanded its capabilities to include merchant payments, in-app purchases, and a Venmo credit card, allowing users to pay directly at participating retailers. These features create multiple potential revenue streams beyond simple transaction fees. While currently under-monetized compared to its scale, Venmo represents a strategic growth engine for PayPal, enabling the company to tap into social payments, attract a younger audience, and experiment with new financial products. Its integration with PayPal’s broader ecosystem further strengthens network effects, positioning Venmo as a key driver of both user engagement and long-term growth.

OPEN AI COLLABORATION

PayPal’s collaboration with OpenAI represents a strategic move to integrate advanced AI capabilities into its payment ecosystem. By leveraging AI technology, PayPal aims to enhance fraud detection, optimize transaction processing, and improve customer experience through smarter insights and automation. This partnership also opens opportunities for more personalized financial services, such as AI-driven spending recommendations or credit assessments. While still in early stages, the collaboration signals PayPal’s commitment to innovation and staying at the forefront of technological advancements in digital payments, positioning the company to better compete in a rapidly evolving fintech landscape.

-

Enhanced Fraud Detection and Security: By integrating advanced AI models, PayPal can more effectively detect suspicious activity, reduce fraud losses, and strengthen trust with both consumers and merchants.

-

Operational Efficiency: AI can automate routine processes, optimize transaction routing, and improve risk management, potentially lowering costs and increasing margins.

-

Personalized Customer Experiences: PayPal could leverage AI to offer tailored financial recommendations, smarter credit assessments, and more engaging user interactions, increasing engagement and retention.

-

Innovation and Competitive Positioning: Partnering with a leading AI company signals PayPal’s commitment to technological leadership, helping it stay ahead of competitors in the fast-evolving fintech sector.

-

New Revenue Opportunities: Advanced AI capabilities could enable PayPal to develop new products or services, such as AI-driven lending, smarter BNPL offerings, or predictive merchant tools, opening additional streams of income.

In short, this agreement could strengthen PayPal’s technology edge, improve operational performance, enhance the user experience, and potentially create new avenues for growth.

OPEN AI x PAYPAL PARTNERSHIP

BNPL; BUY NOW, PAY LATER

PayPal’s Buy Now, Pay Later (BNPL) service has emerged as a key growth driver in its payments ecosystem, offering consumers the ability to split purchases into interest-free or low-interest installments. This approach appeals particularly to younger generations, such as Millennials and Gen Z, who increasingly favor flexible, digital-first financing options over traditional credit cards. As e-commerce continues to expand globally, BNPL has the potential to capture a growing share of consumer spending, positioning PayPal as a preferred partner for both online and in-store merchants.

For merchants, BNPL can drive higher conversion rates, larger average order values, and increased customer loyalty, creating a mutually beneficial dynamic that strengthens PayPal’s network effects. For consumers, it enhances purchasing power without the immediate financial burden, fostering engagement and repeated use of PayPal’s ecosystem. Looking forward, the service could expand into new geographies and verticals, including travel, subscription services, and higher-ticket items, further broadening its reach and relevance.

From a financial perspective, BNPL generates revenue primarily through merchant fees, while consumer fees, such as late or interest charges, provide additional upside. However, as the segment grows, PayPal will need to carefully manage credit and regulatory risks, including potential defaults and tightening of lending rules. Successfully navigating these challenges could solidify BNPL as a long-term strategic advantage, deepening user engagement, increasing transaction volumes, and creating new avenues for monetization across PayPal’s broader ecosystem.

BUY NOW, PAY LATER (BNPL)

PAYPAL ADS

PayPal Ads represents a relatively new and strategic initiative aimed at creating an additional revenue stream while enhancing the engagement of its ecosystem. The idea is to allow merchants to promote their products and services directly within PayPal’s platform, including Venmo, merchant checkout flows, and potentially other parts of the app experience. By leveraging the platform’s vast and highly engaged user base, PayPal Ads can offer merchants a targeted way to reach consumers who are already in a transactional mindset, increasing the likelihood of conversions. From a business perspective, this initiative is significant for several reasons.

-

First, it diversifies PayPal’s revenue beyond traditional transaction fees and financial services, tapping into the lucrative digital advertising market.

-

Second, it strengthens the network effect as more merchants advertise, users may discover new products and services, further incentivizing engagement with PayPal and Venmo.

-

Third, PayPal can leverage its rich transaction and behavioral data to offer highly personalized ad targeting, which can improve campaign effectiveness and command higher advertising fees.

In the long term, PayPal Ads could evolve into a major growth level, especially as e-commerce continues to expand and merchants increasingly seek integrated advertising solutions that connect directly to payments. By combining its core payment services with advertising capabilities, PayPal positions itself not just as a payments processor, but as a platform that can drive both commerce and marketing results, creating a more holistic value proposition for merchants and reinforcing its stickiness with users.

LAST BUT NOT LEAST, $PYUSD STABLECOIN

PayPal’s $PYUSD stablecoin represents a strategic move into the digital currency space, aiming to bridge traditional finance with blockchain-based payments. Designed to maintain a 1:1 peg with the U.S. dollar, $PYUSD offers users a secure, stable digital currency for transactions, remittances, and merchant payments within the PayPal ecosystem. By integrating a stablecoin, PayPal can enable faster, cheaper cross-border payments, reduce reliance on traditional banking rails, and provide new ways for consumers and merchants to transact digitally.

From a strategic standpoint, $PYUSD positions PayPal as a credible player in the growing crypto and decentralized finance market, allowing it to compete with other digital payment providers exploring blockchain solutions. It also complements existing offerings such as Venmo and BNPL, potentially enabling seamless crypto-to-fiat payments or new financial products. While adoption and regulatory considerations remain key challenges, the introduction of $PYUSD reflects PayPal’s commitment to innovation and its ambition to evolve beyond traditional digital payments, creating a more versatile, future-ready platform for consumers and businesses alike. PayPal’s $PYUSD stablecoin has the potential to generate revenue in several ways, although the scale and timeline are still evolving.

-

Transaction Fees: Similar to other digital payments, PayPal can earn small fees on transfers, conversions between fiat and $PYUSD, and payments made to merchants. Even if fees are modest, the high volume of PayPal’s user base could make this a meaningful revenue stream over time.

-

Interest on Reserves: Stablecoins are typically backed 1:1 with fiat reserves. PayPal can earn interest on these reserves by holding them in short-term, low-risk instruments, similar to how other stablecoin issuers generate yield.

-

Merchant Integration & Network Effects: As merchants accept $PYUSD for payments, PayPal may capture additional transaction revenue, similar to its traditional merchant processing fees, while driving higher engagement across its ecosystem.

-

Financial Services Expansion: $PYUSD can enable new offerings like programmable payments, instant settlement, or crypto-linked BNPL products, opening further monetization opportunities.

Circle (USDC) and Tether (USDT) primarily generate revenue through interest on reserves and fees from institutional partners, rather than retail transaction fees. Their business models are largely focused on serving crypto markets and exchanges. PayPal, in contrast, can leverage an existing large retail base and merchant network, giving $PYUSD immediate utility for everyday transactions, not just trading or institutional purposes. This could make its revenue more diversified and tied directly to payment flows rather than reserve interest alone.

In short, while other stablecoins largely monetize via institutional financial flows, $PYUSD has the potential to combine transaction fees, merchant adoption, and interest income, creating a uniquely integrated revenue stream that ties stablecoins directly into everyday consumer and merchant activity.

PYUSD - YOUTUBE PARTNERSHIP

YouTube has begun allowing eligible U.S. creators to receive their earnings, including ad revenue, memberships, and Super Chat payouts in PayPal’s dollar‑pegged stablecoin, PYUSD, via its existing payout infrastructure with PayPal. The feature, confirmed by PayPal’s head of crypto and verified by Google, is currently limited to creators in the United States and builds on PayPal’s broader rollout of PYUSD payout options earlier in 2025.

From a strategic perspective, this move represents a notable step in mainstream crypto integration and enhances PayPal’s role in the creator economy. By offering near‑instant settlements and reduced reliance on traditional banking rails, PYUSD payouts can improve cash flow and lower friction, especially for international creators and those underserved by conventional financial systems. This also boosts PYUSD’s utility and adoption, potentially expanding its network effects and reinforcing PayPal’s position in digital payment rails without YouTube needing to handle crypto directly.

WHO MAKES IT WORK

Alex Chriss, PayPal’s CEO, has been leading the company with a clear vision of transforming it from a traditional digital payments provider into a comprehensive, technology-driven financial ecosystem. Since taking the helm, Chriss has focused on diversifying revenue streams, enhancing user engagement, and expanding the company’s reach through initiatives such as Venmo, BNPL, and the new $PYUSD stablecoin. He has emphasized leveraging emerging technologies (including AI and blockchain) to improve transaction security, optimize operational efficiency, and create innovative financial products that cater to evolving consumer and merchant needs.

Under Chriss’s leadership, PayPal has also pursued strategic partnerships, such as the collaboration with OpenAI, and has introduced new monetization avenues like PayPal Ads, reflecting a proactive approach to staying competitive in an increasingly crowded fintech landscape. His strategy balances growth with disciplined capital allocation, ensuring that expansion efforts are complemented by initiatives that return value to shareholders.

Demonstrating this alignment, Chriss has personally purchased a significant number of PayPal shares recently, signaling strong confidence in the company’s future and a tangible commitment to shareholder interests. This combination of visionary leadership, focus on innovation, and personal investment underscores Chriss’s dedication to positioning PayPal for long-term growth and sustained relevance in the global digital payments market.

ALEX CHRISS (CEO)

BALANCE SHEET

PayPal currently holds a very strong liquidity position, with around $13.7 billion in cash, cash equivalents, and short-term investments as of mid-2025.This sizeable cash pile gives PayPal flexibility to fund operations, invest in new strategic initiatives, and return capital to shareholders without relying too heavily on external financing.

On the liability side, PayPal carries a long-term debt of roughly $11.5–12.6 billion. When you compare that debt to its liquid assets, its net debt is quite manageable, PayPal is not over-leveraged, especially given its ability to generate strong cash flows.

That said, PayPal’s stock-based compensation is a non-trivial expense. In the first half of 2025, it reported around $573 million in stock-based compensation, and its trailing-twelve-month figure is in the ballpark of $1.1 billion. This is fairly common in fintech firms, but it does mean some dilution for shareholders, that the later compensate repurchasing shares, although the expense also helps align employees’ incentives with long-term company performance.

SHAREHOLDER REMUNERATION

PayPal’s management team has consistently demonstrated strong alignment with shareholder interests, emphasizing strategies that enhance long-term value. The leadership’s approach reflects a focus on disciplined capital allocation, balancing investments in growth initiatives with returning cash to shareholders. This alignment provides investors with confidence that decisions are being made to support both the company’s strategic objectives and shareholder returns.

A key example of this alignment is PayPal’s ongoing share repurchase program. Over the years, the company has executed substantial buybacks, effectively reducing the number of outstanding shares and increasing earnings per share. These repurchases not only signal management’s confidence in the business but also provide a direct mechanism to return value to shareholders, reinforcing their commitment to investor interests.

In addition to buybacks, PayPal recently announced a new dividend in its Q3 2025 report. This marks a continuation of the company’s efforts to reward shareholders with a portion of its free cash flow, complementing repurchases and further demonstrating the management’s shareholder-oriented approach. By utilizing its cash to both repurchase shares and initiate dividends, PayPal’s leadership shows a clear dedication to enhancing shareholder value while maintaining flexibility to invest in the company’s growth and innovation.

TOOLS THAT WE USE TO MAKE THIS HAPPEN

These are some of the tools we use for investing, and we've reached an agreement to collaborate with them by adding a discount if you sign up directly from our website. This gesture will also help us remain focused on providing you with the best possible educational content about the stock market.

POTENTIAL RISKS

PayPal faces several challenges that could impact its growth and stability. Factors such as competitive pressures, evolving financial regulations, shifts in digital commerce, technological vulnerabilities, and exposure to credit products may influence its future performance.

-

Intense Competition: PayPal faces strong competition from traditional banks, credit card networks, and emerging fintechs like Stripe, Square, and regional digital wallets. Increased competition could pressure transaction fees and slow user growth.

-

Regulatory and Compliance Risk: Operating in multiple countries exposes PayPal to a complex web of financial regulations, data privacy laws, and anti-money laundering requirements. Non-compliance or regulatory changes could result in fines, operational restrictions, or increased costs.

-

Dependence on e-Commerce Trends: A significant portion of PayPal’s volume comes from online shopping. Any slowdown in e-commerce growth, shifts in consumer behavior, or macroeconomic downturns could reduce transaction volumes and revenue.

-

Technology and Cybersecurity Risks: As a digital payments platform, PayPal is a target for cyberattacks and fraud. Security breaches or technical failures could damage trust, lead to financial losses, and increase spending on cybersecurity measures.

-

Exposure to Credit and BNPL Products: PayPal’s credit and “Buy Now, Pay Later” offerings expose it to credit risk. Higher default rates, economic stress, or poor underwriting decisions could negatively impact earnings and capital requirements.

FAIR VALUATION FOR PAYPAL

A fair valuation for PayPal requires focusing on its underlying fundamentals, cash-flow generation, and long-term strategic positioning. Today, PayPal trades at a much lower earnings and free-cash-flow multiple than during its peak years, largely because investor sentiment remains affected by the 2021 bubble and slowing user growth. However, the company still produces strong free cash flow, maintains a large and profitable branded-checkout franchise, and is expanding into higher-potential areas such as advertising, AI-enhanced services, BNPL, and digital assets.

Given its current growth profile and strong free-cash-flow generation, should reasonably trade at a PER (P/E ratio) in the range of 16–22x, similar to other mature but still innovative fintech companies. Overall, this valuation range represents a fair and grounded assessment of the company’s future earnings potential.